Why it's important to meet your 401(k) match

In an effort to help strengthen the financial health and wellness of their workforces, many employers offer financial benefits for their employees. Some common types of financial wellness benefits are: bonuses, paid time off, retirement account, and a 401(k) match.

For the purposes of this article, we’re going to provide an example of 401(k) matching and demonstrate why it’s important to try and meet your company match.

Why is it important to meet your company 401(k) match?

Perhaps not surprisingly, not everyone meets their 401(k) match. In fact, according to data from our recent Empowering America’s Financial Journey annual report, 29% of people aren’t taking full advantage of their company match.1

If you’re able, meeting your company match is generally a good idea. There’s a reason a 401(k) match is often referred to as “free money.” You don’t have to do anything to earn it other than contribute to your retirement plan; if you contribute to your 401(k), your employer also contributes funds. Knowing how your match works is a key piece of understanding your 401(k) plan.

If your retirement plan offers matching, many companies will typically match 50% or 100% of your contributions up to a certain percentage of your salary. Employer matches are typically made each payroll period, but some employers may make them annually instead.

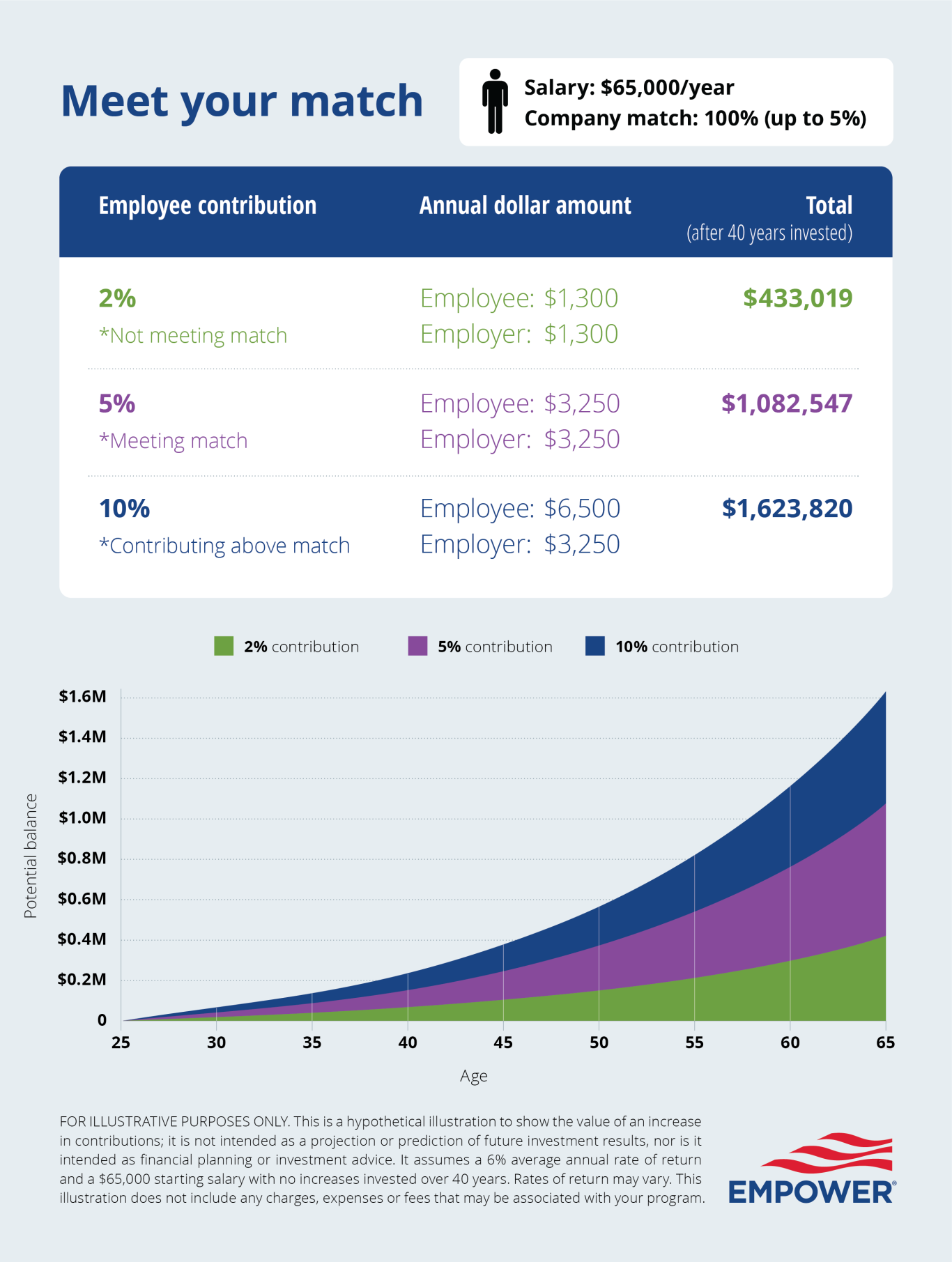

Example of a partial match: 50% of what you contribute up to 6% of your salary. In this scenario, if you earn $100,000 per year and you contribute 6% of your salary, or $6,000, your employer will match and contribute half of that, or $3,000.

Example of a full match: 100% of what you contribute up to 6% of your salary. In this scenario, if you earn $100,000 per year and contribute 6% of your salary ($6,000), your employer will match and contribute the same amount, or $6,000 in this case.

Read more: How does 401(k) matching work?

So now that you understand how a 401(k) match generally works, and why it’s often referred to as “free money,” let’s look at how this could potentially affect your retirement savings over time.

401(k) contribution and matching examples:

The above examples are all about meeting (or even going beyond) your company match. But you don’t have to stop there. Remember, the IRS sets annual contribution limits for 401(k)s and other retirement accounts.

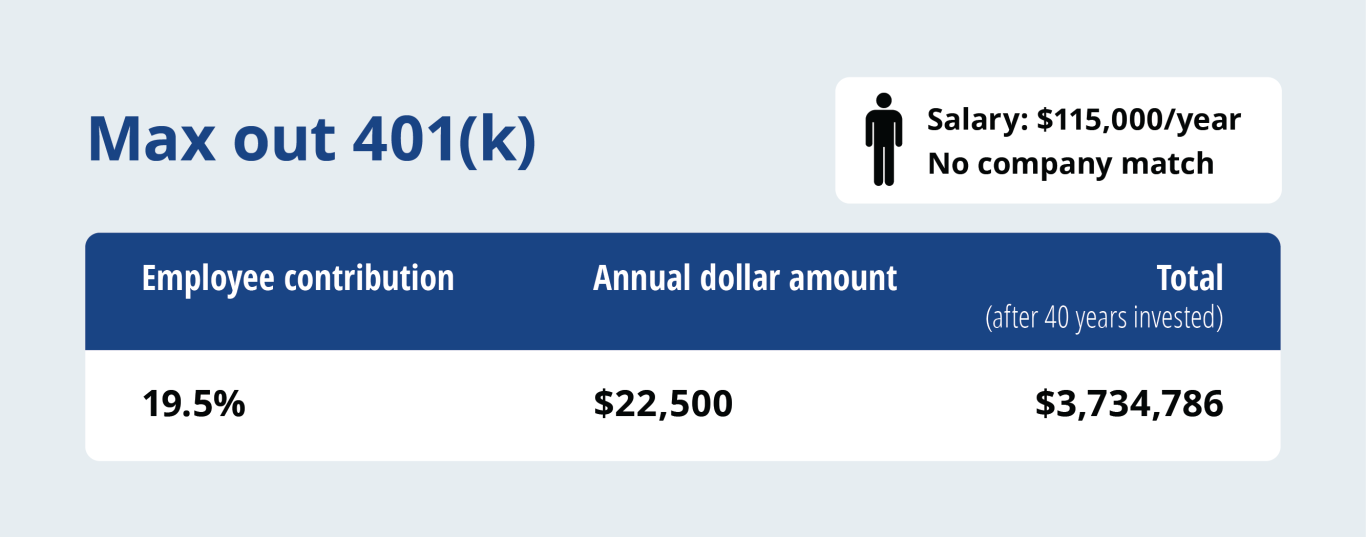

If you were to “max out” your 401(k) in 2023, that would mean you would contribute the IRS contribution limit of $22,500. And thanks to catch-up contributions, employees age 50 or older can contribute up to $30,000 to their 401(k). Keep in mind, this contribution limit is separate from any potential company contributions (like a 401(k) match).

But what if your employer doesn’t offer a match? You can still aim to contribute as much as you can to your 401(k) – and potentially even max it out. Here’s why you might want to consider it:

Why max out your 401(k) if you don’t have an employer match?

FOR ILLUSTRATIVE PURPOSES ONLY. This is a hypothetical illustration to show the value of an increase in contributions; it is not intended as a projection or prediction of future investment results, nor is it intended as financial planning or investment advice. It assumes a 6% average annual rate of return, $115,000 starting salary with no increases invested over 40 years. Rates of return may vary. This illustration does not include any charges, expenses or fees that may be associated with your program.

Every person must decide how much they can realistically contribute to a retirement plan given their unique financial situation. Even if you’re not able to max out your 401(k), then a good goal may be to contribute the minimum amount required to take full advantage of your company match.

Next steps:

Analyze your retirement readiness. Personal Asset offers a tool called the Retirement Planner, which allows you to see how likely your current portfolio and retirement plan are to be successful. You can test out different scenarios to see how different expenses, timelines, or potential company matches may impact your retirement plan.